Originally posted at CalPensions.

By Ed Mendel.

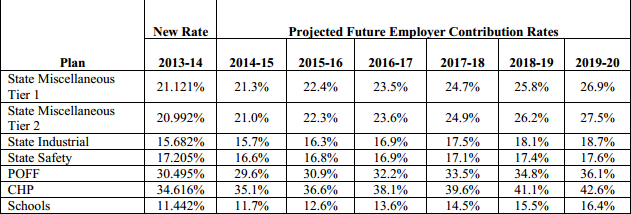

A new CalPERS projection shows employer rates for the largest group of state workers increasing 27 percent over the next six years — but the focus is on the risk of how much things can change.

As the giant pension fund begins to take a bigger bite of state and local government budgets, employers will get more information about rates and a kind of mixed message.

The goal is make rates more predictable for employers, avoiding shocks and allowing time to adjust budgets, while also encouraging employers to think about risks that could change the rates.

A new annual “actuarial valuation” for state and schools plans has added a “risk analysis” section. How rates can change is shown with several examples of different annual investment earnings and long-term earnings forecasts.

CalPERS also is holding a two-day asset liability management workshop next month. It’s open to the public, and representatives from the 1,576 state and local government agencies in CalPERS are encouraged to attend.

“They need to think not just about their current risk levels, but also how that risk level can change over time,” Alan Milligan, CalPERS chief actuary, said last week. “If they are uncomfortable with the risk level now, and we know that is likely to increase, then that’s something they should be aware of and thinking about.”

As pension systems move toward full funding (the goal of new higher CalPERS rates) year-to-year jumps in employer rates are more likely. “Volatility” grows with increasing assets. If there is an investment loss, a bigger rate increase is needed to fill a bigger gap.

Milligan previously has said that a rate increase is likely to result from a review early next year of economic and demographic forecasts, including new projections that people on average are living longer.

Another rate increase could result from a California Public Employees Retirement System board review of asset allocations later this year. Milligan said he is likely to recommend lowering risk levels.

In the past, CalPERS has adopted a “discount rate” to offset future obligations based on a slightly lower earnings forecast than actually expected, providing some cushion to reduce risk.

“I am not sure I will be recommending including a margin for adverse deviation (cushion) in the future,” Milligan said. “I may instead recommend that they consider adopting a less volatile asset mix, because that may be actually a better way to control risk.”

Milligan said the November workshop will consider “flexible derisking.” In a year with outstanding investment returns, for example, the board could think about lowering the discount rate, changing the asset allocation mix or doing both.

New CalPERS projection of state and school rates over next six years (Rates are percentage of pay)

At the core of CalPERS risk is the need to get about two-thirds of the money to pay future pensions from market-based investment earnings, which are difficult if not impossible to predict with precision.

Public pensions in California originally were limited to more predictable investments: bonds. But Proposition 1 in 1966 allowed 25 percent of investments in blue-chip stocks. Proposition 21 in 1984 removed the lid, allowing anything “prudent.”

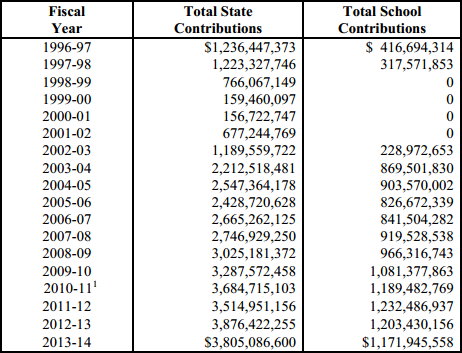

When a booming stock market in the late 1990s gave CalPERS a surplus, pushing the funding level past 100 percent, the pension system followed the common practice of spending the “windfall” rather than keeping the money to offset future downturns.

Employers were given a contribution “holiday,” dropping the annual state payment from $1.2 billion to $159 million in fiscal 1999-00 and to $157 million the following fiscal year. Pension reform legislation last year bans contribution holidays.

CalPERS sponsored a large retroactive pension increase for state workers, SB 400 in 1999, telling legislators “superior” market-based investment returns would cover the cost.

The SB 400 benefit increase accounted for 27 percent of the increase in the annual state CalPERS payment by fiscal 2009-10, a chart on the CalPERS Responds website said several years ago. The pension reform rolled back the SB 400 increase for new hires.

A provision in SB 400 allowed local police to bargain for the trendsetting 50 percent pension increase given the Highway Patrol. Critics say big police and firefighter pensions, matching the Highway Patrol increase, are straining local government budgets.

As state payments to CalPERS soared, reaching $2.5 billion in fiscal 2004-05, former Gov. Arnold Schwarzenegger briefly backed a proposal to switch state and local government new hires to 401(k)-style individual investment plans.

CalPERS announced a new actuarial method in 2005 aimed at preventing future rate shocks. A radical “smoothing” plan spread investment gains and losses over 15 years, well beyond the three to five years used by most public pensions.

When a deep recession hit, the CalPERS investment fund plunged from about $260 billion in the fall of 2007 to $160 billion in March 2009. The CalPERS fund, which did not reach $260 billion again until this year, was valued at $270.5 billion last week.

The big loss revealed shortcomings in the 2005 actuarial method that kept rates low. CalPERS in 2009 temporarily lifted actuarial limits for a three-year phase in of the biggest one-year loss, $24 billion.

Other problems are described in an annual risk report this year. For example, most funds pay less than the annual interest on their debt or “unfunded liability” and state funding levels have a better than even chance of dropping below 50 percent.

CalPERS took one step to raise employer rates in March last year by lowering the discount rate from 7.75 to 7.5 percent. Critics say the earnings forecast is still too optimistic.

Another step raising rates came last April when CalPERS adopted a new actuarial method aimed at getting to full funding. The estimate then was that rates could go up roughly 50 percent over the next seven years.

Now the next step could be a change in investment policy as the board looks at asset allocations later this year.

CalPERS has about 70 percent of the projected assets needed to pay future pension obligations. The prospect of another economic downturn, and more heavy investment losses, is worrisome.

“There is a substantial risk that, at some point over the foreseeable future, there will be periods of low funded status and high employer contribution rates,” said the risk report issued this year before the new actuarial methods were adopted.

“Should this coincide with a period of financial weakness for employers or if such a period occurs before we recover from the current funding shortfall, the consequences could be very difficult to bear.”