Originally posted at CalPensions.

By Ed Mendel.

A new study shows CalPERS members are living longer. It’s the first step in a review of workforce changes and investment polices that could lead to higher contribution rates for employers and possibly employees.

After years of keeping employer rates low, CalPERS in April switched from an actuarial method that spread investment gains and losses over 15 years to a more direct method, boosting employer rates roughly 50 percent over the next seven years.

Now the next phase of a CalPERS plan to reach full funding looks at three things that could push rates even higher: investment allocation, earnings forecast used to offset or discount pension obligations and demographic changes including mortality.

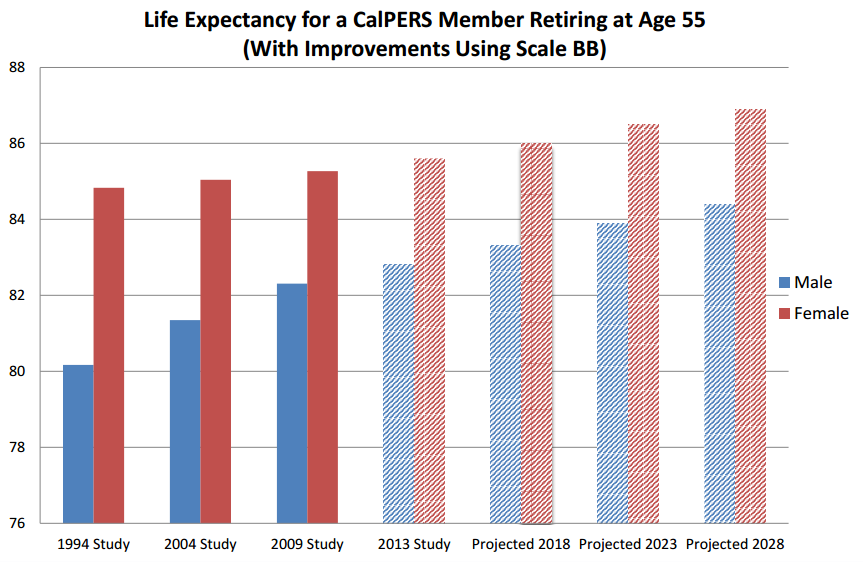

“Over the last 20 years or so life expectancy for a new retiree has gone up about 2½ years for males and about one year for females,” the CalPERS chief actuary, Alan Milligan, told a board workshop on mortality projections last month.

Life spans have been steadily increasing since the turn of the last century. A new mortality improvement scale issued by the Society of Actuaries last year reflects the latest rise in longevity, which could trigger a boost in employer pension rates to cover the cost.

The new “scale BB” widely used by public pensions is based on Social Security data. At CalPERS, a new 1997-2011 experience study shows members “significantly exceed” the new Social Security-based scale, possibly calling for an even higher rate increase.

“I can tell you this graph is giving me a bit of heartburn in terms of what to recommend in the way of future mortality improvements,” Milligan said, referring to one of the slides shown the board during the presentation.

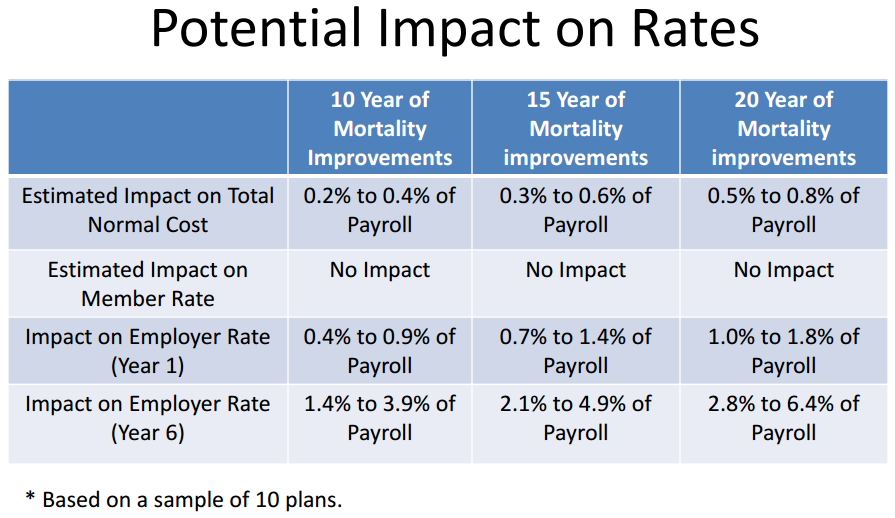

The structure of 2,000 separate CalPERS plans vary. So increasing the estimated time retirees will receive pensions yields a range of results. At the workshop, the board was shown potential rate increases based on a sample of 10 plans.

Assuming 10 years of mortality improvement, a phased-in employer rate increase would be 0.4 percent to 0.9 percent of pay in the first year and in the sixth year 1.4 percent to 3.9 percent of pay.

Assuming 20 years of mortality improvement, the employer rate increase would be 1.0 percent to 1.8 percent of pay in the first year and in the sixth year 2.8 percent to 6.4 percent of pay.

Under a pension reform Gov. Brown pushed through the Legislature last year, a new concern for the labor-friendly CalPERS board is the possibility of raising employee contributions.

The reform calls for a 50-50 split of the pension “normal cost,” the price of pensions earned during a single year. Under the CalPERS view of the new law, a normal cost increase of a full 1 percent of pay is needed to trigger an employee rate increase.

In the sample of potential rate increases from mortality improvements, there is “no impact” on member or employee contributions. The normal cost increases, but not by a full 1 percent.

For most state workers (“miscellaneous” Tier 1), for example, employers contribute 21 percent of pay to CalPERS and employees contribute 8 percent of pay. The “normal cost” of the plan is 15 percent of pay.

The rest of the total contribution, paid entirely by the employer, is for the debt or “unfunded liability.” It’s mainly due to investment earnings that fall below the forecast, particularly heavy losses during the recent recession.

Investment earnings are expected to cover about two-thirds of future pension costs. As of June 30 last year, the state worker plan had 66 percent of the projected assets needed to pay future pensions and an unfunded liability of $28 billion.

Employee pension contributions, which take a bite out of the paycheck, can be a major labor issue. As employers try to control the rising costs of legally protected pensions, one of their few options is getting employees to share more of the cost.

Former Gov. Arnold Schwarzenegger held up the state budget for a record 100 days in 2010 in a battle that resulted in the largest state worker union raising its pension contribution from 5 percent to 8 percent of pay.

In what some call a “pension pickup,” many local governments have been paying the employee pension contribution. The new pension reform bans “employer paid member contributions” for new hires.

Although CalPERS is not expecting a mortality improvement alone to trigger an increase in the employee contribution, a review of other possible changes is scheduled for December that could increase the normal cost.

“We are still reviewing the other assumptions, but we don’t know yet if the combination of all the changes would trigger a change of more than 1 percent,” David Lamoureux, CalPERS deputy chief actuary, told the board workshop. “So, we are still looking at that right now. We will be able to tell you more in December.”

In the plan to reach full funding and make CalPERS sustainable, the board is scheduled to receive preliminary staff recommendations in December for demographic and economic assumptions, before final recommendations and adoption in February.

Among the assumptions are mortality, retirement rates, pay increases, inflation, employment trends, termination, disability and the crucial earnings forecast used to offset or discount future pension obligations.

In December, the CalPERS board is scheduled to act on a recommendation for asset allocation that could influence the discount rate. A two-day board workshop on asset liability management Nov. 12 and 13 will be webcast live.

The CalPERS earnings forecast used to discount future pension obligations was dropped in March last year from 7.75 to 7.5 percent a year. Critics say the earnings forecast is still too optimistic, concealing massive pension debt.

In a mortality forecast, Milligan said, there is “a risk of over or under projecting,” but the increasing longevity is too big to ignore. His recommendation is likely to be based on the new scale BB with some variations.

He said higher CalPERS longevity may be due to things like income, education and access to medical care. One question about projecting improved mortality: To what degree are favorable socio-economic factors offset by the limited ability of the already-low smoking rate in California to decline?

The Actuarial Standards Board concluded that emerging health issues such as obesity and diabetes could slow mortality improvement, but “do not alter the scientific consensus of likely continuing improvements in mortality.”

A well-known technological innovator, Ray Kurzweil, hired by Google earlier this year to work on a kind of artificial intelligence project, has famously predicted that in 15 years life expectancy will be growing each year at the rate of more than a year.

The subtitle of one of his books: “Live long enough to live forever.” Milligan told the workshop the new scale BB expects a certain amount of “medical breakthrough” to improve mortality.

“They are certainly not expecting anything radical,” he said. “If there is a radical breakthrough in the health field — well, we are going to be wrong.”