Still underfunded after a $100 billion loss during the recession, CalPERS plans to slowly shift over decades to more conservative and lower-yielding investments, raising employer rates but reducing the risk of another financial bloodbath.

The Brown administration, repeating a request made in August, again urged the CalPERS board last week to promptly begin phasing in a rate increase over the next five years.

“I think we are missing an opportunity and putting off the day of reckoning, and it may come back to bite us,” said board member Richard Gillihan, Brown’s human resources director.

But the majority of the 13-member board, public employee union members and their allies, support the go-slow “risk mitigation” policy expected to be adopted in November or December after more than 1½ years of study.

“There are public agencies (local governments) that don’t have the money to move forward on a policy to reduce our risk right now,” said board member Theresa Taylor, elected by state workers.

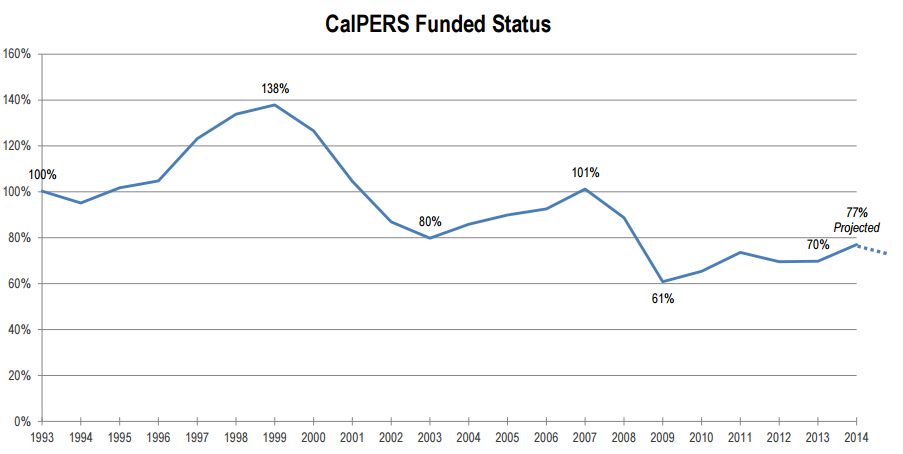

In the fall of 2007, CalPERS had investments worth $260 billion and 101 percent of the projected assets need for future pension obligations. By March 2009, the investments had dropped to about $160 billion and the funding level to 61 percent.

Since then the Standard & Poor’s 500 index of big stocks has nearly tripled. But the California Public Employees Retirement System is only about 74 percent funded now with investments totaling $286 billion at the first of the month.

Experts have told CalPERS that in the maturing system, where retirees are beginning to outnumber active workers, some investment funds are needed to pay pensions, reducing earnings.

“It’s been very challenging to dig out of that hole,” Andrew Junkin, a Wilshire consultant, told the board last August.

CalPERS expects investment earnings to provide about two-thirds of the money needed to pay future pensions, with the rest coming mainly from employer contributions and a lesser amount from employees.

Critics say the CalPERS earnings forecast, now 7.5 percent, is too optimistic and overstates the projected funding level, concealing massive debt. The investments needed to support an optimistic earnings forecast have a higher yield because they are riskier.

For example, government bonds yield a certain amount with little risk of an investment loss. Stocks that can produce much bigger yields than bonds are more risky, because they also can yield big losses.

The risk mitigation policy shifts the focus from whether employer-employee rates are high enough to properly fund the system. The new policy seeks more investments that reduce the risk of another big loss and an even harder-to-dig-out-of hole.

The CalPERS board has been told that experts think if the funding level drops low enough, perhaps around 40 to 50 percent, it becomes impractical to push rate increases and earnings forecasts high enough to project full funding.

“If we have another event similar to ’08-09 then we reach a point where we can’t recover,” board member Bill Slaton, a Brown appointee representing local government elected officials, said at the meeting last week. “That’s what the industry tells us.”

The risk mitigation for a maturing CalPERS is long-term for several reasons. The amount of investments diverted to pay pensions will continue to increase. In two decades, poor investment earnings will require a proportionately larger rate increase than today.

Action now could result in another employer rate increase, putting more strain on local government budgets already facing a total rate increase of roughly 50 percent that is still being phased in.

Last year employer rates intended to get CalPERS to full funding in several decades were at record highs for some plans. Rates exceeded 30 percent of pay for more than 100 miscellaneous plans and 40 percent of pay for more than 150 safety plans.

“Employers are reporting that these contribution levels are putting significant strain on their budgets and limiting their ability to provide services to the people in their jurisdictions,” the annual CalPERS risk andfunding report said last November.

The risk mitigation plan avoids a direct employer rate increase. In a year when earnings exceed the 7.5 percent forecast by at least 4 percent, half of the excess would be used to lower the forecast by 0.05 percent, allowing a shift to less risky investments.

The other half of the excess would be used to lower the employer rate, canceling out the rate increase that would otherwise result from lowering the earnings forecast needed to project full funding.

But in the long run, the risk mitigation is expected to indirectly increase employer rates because some of the excess from good years would be skimmed off, leaving less to offset the rate increase needed for years when earnings fall below the forecast.

This technical issue came up last week when Slaton suggested lowering the threshold for risk mitigation from earnings that are 4 percent above the forecast to 2 percent.

Alan Milligan, the CalPERS chief actuary, said lowering the threshold to 2 percent could result in a direct employer rate increase. He said excess earnings of at least 2 percent are needed to offset the rate increase resulting from a lower earnings forecast.

The plan to split the excess earnings, rather than use it all for risk mitigation, reflects the view of some board members who want employers to benefit from good investment years.

A staff report last week said the largest state worker union, SEIU, wants a policy requiring a board vote before risk reduction is triggered in a year with excess earnings. The staff believes the board already has that flexibility.

Among the 3,093 local governments in CalPERS there is a wide range of funding levels and employer rates. Some are contributing more than the required CalPERS rate to pay down their debt or “unfunded liability.”

Milligan said plans that are more than 100 percent funded cannot use the surplus to reduce their “normal cost,” which covers the pension earned during a year but not the debt from previous years.

A pension reform requires employers to contribute at least half of the annual normal cost. Milligan said CalPERS is considering creating a “pension prefunding trust” to help employers with a surplus lower their cost.

Board member J.J. Jelincic, elected by active and retired CalPERS members, is skeptical of the risk mitigation plan. He said earnings averaging 7.5 percent are “highly doable” over a long period.

Jelincic said he knows CalPERS staff is aware of academic work suggesting a more effective way to reduce risk would divide investments into a “hedging” portfolio and a “risk return” portfolio. He asked why the option was not presented to the board.

Ted Eliopoulos, the CalPERS chief investment officer, said the two-portfolio risk reduction method is being explored by the staff for discussion during the next round of asset allocation in about 2½ years.

“It would be a departure from our current asset allocation mix and wasn’t considered as an option for the risk mitigation process we have just gone through,” said Eliopoulos.

[divider] [/divider]