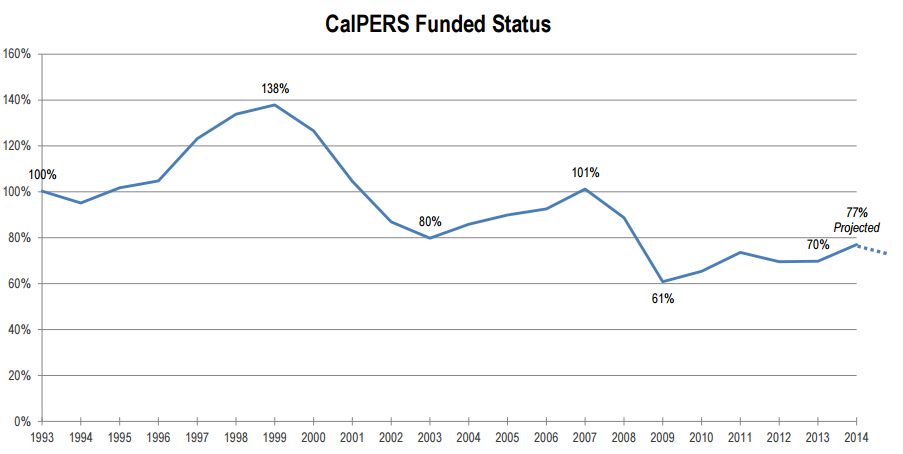

Twice in recent decades CalPERS fell below 100 percent of the funding needed for promised pensions, and twice CalPERS climbed back. But since a $100 billion investment loss in 2008, the CalPERS funding level has not recovered.

Now with about 75 percent of the projected assets needed to pay future pensions, CalPERS has had low investment earnings during the last two fiscal years. Experts expect the trend to continue during the next decade.

“We have some challenges to confront in what is, both for ourselves and all institutional investors, moving into a much more challenging low-return environment,” Ted Eliopoulos, CalPERS chief investment officer, told reporters last month.

If the investment fund earnings that are expected to pay two-thirds of future pensions remain low, the annual payments to CalPERS from state and local governments may continue to grow.

So far, the CalPERS board has resisted Gov. Brown’s calls to raise rates even higher, citing the pressure on local government budgets of recent rate increases. The last one, covering longer lives expected for retirees, is still being phased in.

Many employer rates are already at an all-time high. For 80 miscellaneous plans, rates are over 30 percent of pay. For 135 police and firefighter plans, rates are over 40 percent of pay.

“Employers are reporting that these contribution levels are putting significant strain on their budgets and limiting their ability to provide services to the people in their jurisdictions,” the annual CalPERS funding and risk review said last November.

Low earnings also would undermine a new CalPERS “risk mitigation” strategy that over the decades could very gradually, without triggering a major rate increase, reduce the current earnings forecast, 7.5 percent a year, which critics say is too optimistic.

When earnings are 11.5 percent or higher, the strategy switches half of the money above 7.5 percent to investments with lower yields but less risk of loss. The CalPERS board rejected a Brown aide proposal for a five-year phase in of a 6.5 percent forecast.

After the CalPERS board adopted the risk mitigation strategy last November, Brown said in a news release: “This approach will expose the fund to an unacceptable level of risk in the coming years.”

Some CalPERS board members and union officials predicted CalPERS would once again recover when investments plunged from $260 billion in the fall of 2007 to $160 billion in March 2009, dropping the funding level from 101 percent to 61 percent.

But among the differences this time, in addition to the size of the loss, were low interest rates, stagnant or shrinking payrolls, a wave of Baby Boom retirements, and a maturing fund with negative cash flow requiring the sale of investments to pay pensions.

When the funding level remained low after a lengthy bull market in stocks, which are half of the CalPERS fund valued at $302 billion last week, board members began to mention a new threat.

The board has been told by experts that if the funding level drops low enough, perhaps around 40 to 50 percent, pushing rate increases and earnings forecasts high enough to get back to full funding becomes impractical.

The investment earnings CalPERS reported for the fiscal year ending June 30 were a scant 0.61 percent, lower than the 2.4 percent earned the previous year. The two lean years followed two good years of double-digit earnings, 17.7 and 12.5 percent.

Markets, like most things happening in the future, tend to be difficult to predict with certainty. In the famous quip of the distinguished economist Paul Samuelson: “Wall Street indexes predicted nine out of the last five recessions.”

The earnings forecast or “capital market assumptions” adopted by CalPERS two years ago was 7.1 percent during the next 10 years, Eliopoulos told reporters last month. Now Wilshire and other consultants have dropped their 10-year forecast to 6.64 percent.

“We quite clearly have a lower expected return expectation than we had just two years ago,” Eliopoulos said. “So that will be reflected in our next cycle, which again will look at a 10-year period.”

A routine CalPERS “asset liability management” process begins next year and will be completed in 2018. If the earnings forecast is lowered, CalPERS presumably faces difficult decisions about raising rates and adding higher-yielding but riskier investments.

“We are cognizant that this is a challenging environment for institutional investors and that we have to work collectively within CalPERS to address these challenges,” Eliopoulos said.

The CalPERS reply to earnings forecast critics has been that its long-term earnings average more than 7.5 percent. But after the two weak years, the three-year CalPERS earnings average is 6.86 percent and the 20-year average 7.03 percent.

In a new nationwide look at public pension funding, CalPERS is about average despite generous pensions it sponsored (SB 400 in 1999) and encouraged (AB 616 in 2001) and placing last five years ago in a Wilshire ranking of investment performance.

The average pension system was 74 percent funded last year with an earnings forecast of 7.6 percent, said a brief by Alicia Munnell and Jean-Pierre Aubrey of the Center for Retirement Research at Boston College using the Public Plans Database.

Why the earnings forecast is at the center of the debate over whether CalPERS and other public pension systems are “sustainable” or need major cost-cutting reform is shown by a chart in the brief.

Using a 7.6 percent earnings forecast to offset or “discount” future pension costs, the funds in the national database have 74 percent of the projected assets needed to pay future pensions and a debt or “unfunded liability” of $1.2 trillion.

But if the earnings forecast is dropped to 4 percent, near the risk-free bond rate some critics say should be used to discount guaranteed pensions, the funding level drops to 45 percent and the unfunded liability soars to $4.1 trillion.

The brief issued in June by Munnell and Aubrey uses italics to emphasize that financial economists argue that a risk-free rate should be used for reporting purposes, apparently implying not for setting employer rates and allocating investments.

“Moreover, even many who agree that the expected return may be appropriate for funding purposes are concerned about the level of assumed returns in the current financial market environment,” their brief added, echoing the remarks by Eliopoulos.

Since the CalPERS funding level last year reported in the database, 74.5 percent, is similar to the 74 percent national average, another chart in the brief shows two possible investment scenarios that might roughly apply to CalPERS, given investment differences.

If investment earnings are the “baseline” average of 7.6 percent, the funding level would by 77.6 percent in 2020. If earnings are the “alternative” average of 4.6 percent, the funding level would be 72.1 percent in 2020.

[divider] [/divider]