CalPERS is considering a step toward buying companies on its own, rather than through partnerships with private equity firms that charge high annual fees and then take a chunk of the profits.

Private equity has been producing higher yields than publicly traded stocks. Under the current CalPERS investment portfolio, private equity is the only asset class expected to yield more than what critics say is an overly optimistic earnings target, a 7 percent average.

If markets decline after a decade-long bull market, as many expect, CalPERS may need a boost to hit not only its earnings target, but also to improve a funding level that last month was only 68 per cent of the projected assets needed to pay future pension costs.

The pitch for a new private equity plan even suggests that more of it could reduce or avoid the need for another employer rate increase. Rates are already at all-time highs, squeezing local government budgets, and are scheduled to go up for another five years.

The proposal to create two private private equity investment companies with “innovative” and “long-term” strategies, run by outside experts not under state salary caps, sounds more like a long-term plan than a quick fix.

New CalPERS chief investment officer, Ben Meng, who began work in January, told the board last month he was glad to hear the staff had adopted a “trial and error” approach to the plan developed during the last two years after extensive research.

“It may or may not work and may or may not work now,” he said. “However, given our current underfunded status and our outlook for the economy, doing nothing is not an option.”

Replying to critics who want an “in-house” staff that could buy companies on their own, like some Canadian public pension funds, Meng said CalPERS lacks the expertise and is not located in a financial center usually desired by top talent as they look for deals.

“Basically, we need to learn how to walk before we can run,” he said.

Meng said CalPERS owes employers and members an exploration of the proposed plan and other solutions before it may be forced to lower the 7 percent earnings forecast used to discount debt, resulting in another employer rate increase.

“So in conclusion, we need private equity, and we need more of it, and we need it now,” Meng told the board. “But we will do it in the most risk-prudent way and in the most risk-intelligent way.”

CalPERS also would try to expand its current private equity program, which could be difficult. It has not been able to buy into enough high-quality private equity funds to meet its investment target.

The CalPERS board was told last month that the pension fund has been “chronically underweight” in its top-earning asset class. Only about 7 percent of the total pension fund valued at $354 billion last week has been invested in private equity, below the target of 8 percent.

Last year the California Public Employees Retirement System invested about $6 billion in 18 private equity funds. CalPERS would need to invest about $10 billion a year to remain at the target of 8 percent of the fund.

Investing $10 billion a year would probably require finding 25 to 30 attactive private equity investments, said Steven Hartt, a Meketa consultant, and that would be a lot for the current private equity “structure to be able to find.”

Increasing private equity demand by large investors has created a glut of buyers and $2.5 trillion in global “dry powder,” money committed to managers not yet spent, Andrew Junkin, a Wilshire consultant, told the board. Top private equity funds can choose investors.

Doubling private equity could lower employer miscellaneous rates

Many public pension systems are underfunded since a market crash in 2008, when CalPERS lost $100 billion. Milliman estimates that the largest 100 U.S. public pension systems were 67.2 percent funded as of Dec. 31, 2018, when CalPERS was 65 to 66 percent funded.

A low funding level, even though the stock market has quadrupled since 2008, leaves the pension systems more vulnerable to an economic downturn or market sell-off that could drop their funding to 50 percent, a red line experts say makes recovery very difficult.

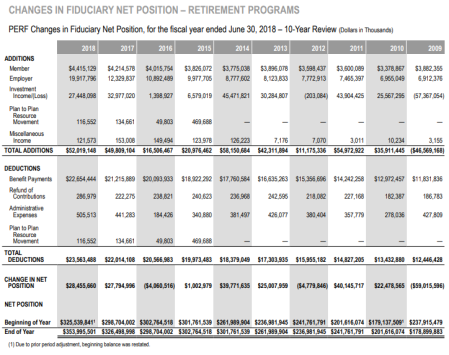

The CalPERS debt or unfunded liability, $139 billion as of last June 30, grows at the rate of 7 percent a year, the interest the debt would have earned if the money was in the investment fund and earnings hit the target.

CalPERS is a mature system with an investment fund several times larger than the employee payroll on which rates are based. So replacing a loss now requires a much larger rate increase than decades ago, when the payroll and fund were about the same size.

After the 2008 crash, CalPERS did not begin rate increases until 2012. Employer payments have nearly tripled from $6.9 billion in 2009 to $19.9 billion last year. Payments by employees, who do not pay for debt, were relatively flat, going from $3.9 billion to $4.4 billion.

The average employer “safety” or police and firefighter rate will reach 49 percent of pay in July, with top rates for 24 local governments of 70 percent or more of pay, a CalPERS funding and risks report said last fall.

CalPERS costs took 11 percent of the average city budget last fiscal year, up from 8.2 percent in fiscal 2006-07, and are expected to take 15.8 percent in fiscal 2024-25, a League of California Cities report said last year.

“In FY 2024–25, 25 percent of cities are anticipated to spend more than 18 percent of their General Fund on CalPERS pension costs with 10 percent anticipated to spend 21.5 percent or more,” said the League report. “These cities are located throughout the state.”

The two new companies would give CalPERS more control over investments. The most lucrative form of CalPERS private equity has been ieveraged buyouts, a type of investment that at times has resulterd in ruthlessly cut jobs, stripped assets, and companies crippled by debt.

CalPERS expects the new companies to provide more “transparency” or knowledge about operations, but that would not be public because of market competition. More private equity also could give CalPERS more protection against big losses in market downturns.

Two retiree groups and a former CalPERS board member, J.J. Jelincic, are skeptical or opposed to the new plan to focus on private equity, citing its declining yields, buyer glut, lack of transparency about pay and fees, and alternatives such as “in-house” private equity and leveraged stock.

But during a public period at the board meeting last month, the CalPERS staff’s four-part private equity plan, including the two new companies, got support from most of the major local government groups and public employee unions.

“It’s not very often that Mr. Brennand and I are agreeing on the same thing,” Dane Hutchings of the League of California said, referring to Terry Brennand of SEIU California. “We think it’s good for the employee. It’s good for the employer.”

A glimmer of good news for CalPERS at the board meeting last month: A Wilshire forecast two years ago, sometimes mentioned by critics, estimating the current CalPERS portfolio would yield 6.2 percent during the next 10 years has been raised to 6.75 percent.

“Over 10 years we think you are going to earn very close to your expected rate of return,” Wilshire’s Junkin told the board, “and recognize we know our forecasts are wrong. That’s one thing I know about them.”

Junkin explained that the forecast is a rational framework, based on fundamentals and risk, but not precise. CalPERS is scheduled to make a four-year adjustment in its investment allocations next year, which could change the earnings forecast and employer rates.

Adoption of the new private equity plan, much of which remains to be fleshed out, may affect the earnings forecast.

CalPERS employer-employee contributions now exceed pension payments

[divider] [/divider]