The state’s two largest public pension systems never recovered from huge investment losses during the deep recession and stock market crash in 2008. CalPERS lost about $100 billion and CalSTRS about $68 billion.

Now after a lengthy bull market, most experts are predicting a decade of weak investment returns, well below the annual average earnings of 7.5 percent that CalPERS and CalSTRS expect to pay two-thirds of their future pension costs.

The two systems are still seriously underfunded, CalPERS at 68 percent and CalSTRS at 65 percent. This is not money in the bank. It’s an estimate of the future pension costs covered by expected employer-employee contributions and the investment earnings forecast.

Last week, the CalPERS and CalSTRS boards got separate staff briefings on how the “maturing” of the two big retirement systems creates new funding difficulties. Both are nearing a time when there will be more retirees in the system than active workers.

The California State Teachers Retirement System board, for example, was told that in 1971 there were were six active workers in the system for every retiree. Today CalSTRS only has 1.5 active workers for every retiree, similar to the CalPERS ratio.

A wave of baby boom retirees that began around 2011, and the continuing increase in the average life span of retirees, have added to the growing cost of paying pensions, giving both systems what actuaries call “negative cash flow.”

The annual cost of paying pensions is more than the annual contributions from employers and employees. So, the pension funds are forced to “eat their seed corn” by selling some investments to cover the gap, thus reducing potential investment earnings.

The California Public Employees Retirement System had about $14 billion in contributions in fiscal 2015-16 and pension payments totaling $19 billion. By 2035, the board was told, contributions are expected to be $17 billion and pension payments $35 billion.

Mature pension funds also have another difficulty. The pension investment fund becomes much larger than the active worker payroll, which means that replacing an investment loss requires a larger employer contribution increase.

The CaSTRS board was told that replacing a 10 percent investment loss in 1975, when the teacher payroll and investment fund were about equal, would have required a contribution increase of 0.5 percent of payroll.

Replacing a 10 percent investment loss today, when the investment fund is six times greater than the payroll, requires a contribution increase of 3 percent of pay. CalSTRS has had losses of 10 percent (below the 7.5 percent forecast) four times in the last two decades.

Both systems recently adopted modest “risk mitigation” strategies to reduce losses. When CalPERS earns 11.5 percent or more, half of the excess will be shifted to conservative investments. CalSTRS is shifting 9 percent of its fund to more conservative investments.

Gov. Brown’s modest cost-cutting pension reform gives new CalPERS and CalSTRS employees hired after Jan. 1, 2013, lower pension formulas, capped at the upper end, and possibly higher contributions. Significant employer savings are decades away.

Meanwhile, CalPERS and CalSTRS are still phasing in record high employer contribution increases. And both will be considering more rate increases in the next several months.

A CalPERS rate increase of roughly 50 percent was enacted in three consecutive years: a lower earnings forecast in 2012, an actuarial method that no longer annually refinances debt in 2013, and a longer average life expectancey for retirees in 2014.

A staff survey of more than 600 CalPERS employers in October and early this month found that most are aware of discussions about another drop in the earnings forecast used to “discount” pension debt.

Nearly two-thirds have begun planning for a rate increase with budget forecasts and 13 percent are “prefunding” by contributing more than the required rate. Their top priorities are less volatile and more predictable rates and a phase-in rather than lump-sum increase.

A League of California Cities lobbyist, Dane Hutchings, told the board the association has no formal position on another rate increase. But he thinks most cities expect an increase and pressure to improve funding after new accounting rules expose more pension debt.

Pensions are needed to help cities remain competitive in the job market, Hutchings said, but another rate increase will be painful for some. “We have cities that are very close to filing for bankruptcy,” he said.

The governor unsuccessfully pushed for a major CalPERS rate increase when the risk mitigation streategy was adopted last year. The CalPERS staff is concerned that its consultant, Wilshire, dropped its 10-year earnings forecast to about 6.1 percent, echoing many experts.

“Given that, we think it’s appropriate for this committee to look at our discount rate,” said Ted Eliopoulos, CalPERS chief investment officer.

A Wilshire consultant, Andrew Junkin, told the board the 30-year earnings forecast is still 7.5 percent or more. But, he added, that assumes there is no major investment loss, like one big enough to cause officials to question whether the state should continue to offer pensions.

“I’ll use this phrase, I don’t mean to be inflammatory, there could be a return that puts you out of business somewhere before you get to year 30,” Junkin said.

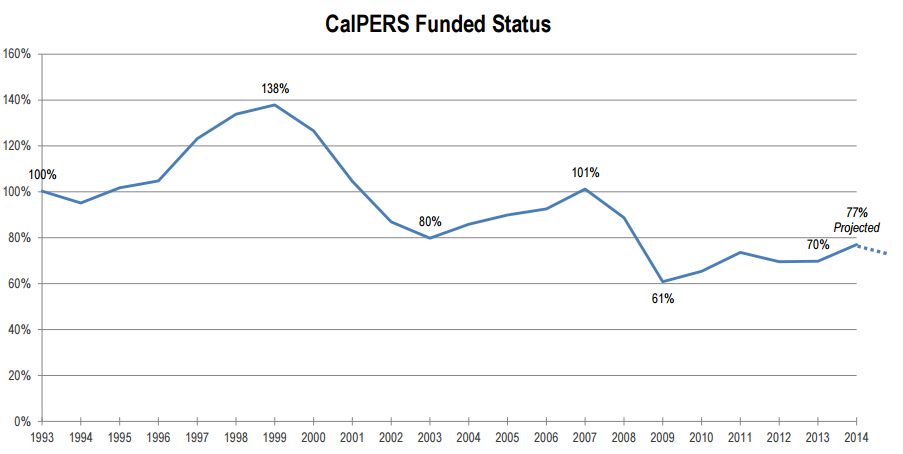

CalPERS was 100 percent funded in 2007 before the stock market crash dropped funding to 61 percent. Experts have told CalPERS, now only 68 percent funded, that if funding drops below 50 percent getting back to full funding could require impractical rate increases and earnings forecasts.

The board was told that a rate increase must be approved by April to take effect for the state and schools in the new fiscal year beginning next July and for local governments in July 2018.

Supporters suggested a rate increase by April would allow a phase in before a recession, if one is on the way, while being fiduciarily responsible. “Pay now or pay more later,” said board member Richard Gillihan, a Brown administration official.

Alarmed union representatives, backed by some board members, urged the board to go slow and follow the regular two-year process leading to a full “asset liability management” review scheduled in 2018.

Dave Low of the California School Employees Association said many non-teaching school workers have not had a pay raise for five or six years. He said if Brown is not putting money in the state budget to offset a rate increase his members could be harmed.

“If you’re not at the table, you’re probably on the menu,” Low said, apparently referring to an old saying about labor bargaining. “We feel like we are on the menu in this discussion.”

With the consent of other board members, Richard Costigan, chairman of the CalPERS fionance committee, directed staff to prepare a report for the December board meeting on a vote for a rate increase by April.

Unique among large California public pension systems, CalSTRS has been unable to raise employer rates, needing legislation instead. That changed with a long-delayed rate increase two years ago that is phasing in a $5 billion rate increase over seven years.

School district rates will more than double, going from 8.25 percent of pay to 19.1 percent by July 2020. Teachers got a small rate increase, going from 8 percent of pay to 10.25 percent for most and to 9.21 percent for teachers hired after the reform on Jan. 1, 2013.

The state rate (a way that CalSTRS remains unique, since other systems only get contributions from employers and employees) is scheduled to go from 5.5 percent of pay to 8.8 percent.

The legislation also gave the CalSTRS board the new power to raise annual rates for the deep-pocketed state, limited to a 0.5 percent of pay each year. And now for the first time, the CalSTRS board is scheduled to consider an annual state rate increase next April.

If the board maximizes its new power, the current state rate of about 6 percent of pay theoretically could go to 21 percent before the legislation expires in 30 years, when the system would be fully funded if investments hit their earnings target, the board was told last week.

The legislation gave the CalSTRS board another new power to annually adjust school district rates beginning July 1, 2021. But the employer rate is capped at 20.5 percent of pay, allowing only small changes in the phased-in rate reaching 19.1 percent by 2020.

“There is no need to increase state contributions further, based on what we have seen to date, even with the 1 percent return last year,” David Lamoureux, a CalSTRS actuary, told the board last week.

The CalSTRS board is scheduled to review “actuarial assumptions” in February, including estimates of the average retiree life span and probably a discussion of the earnings forecast.

“There is a possibility, depending on where we end up with the assumptions, that it could trigger an increase in the normal cost of more than 1 percent (of pay), and it could increase the member contribution rate,” Lamoureux said.

The “normal” cost is the rate for the pension earned during a year, excluding the debt or “unfunded liability” from previous years usually resulting from investment earnings that fall below the forecast.

Under the pension reform, employees are required to pay half of the normal cost when it increases by 1 percent or more.

[divider] [/divider]