By Ed Ring, Executive Director of the California Public Policy Center.

For the first time in the pension fund’s history, we paid out more in retirement benefits than we took in contributions.” – Anne Stausboll, Chief Executive Officer, CalPERS, 2014-2015 Comprehensive Annual Financial Report

There are few examples of a seemingly innocuous statement with more significance than Stausboll’s admission, buried within her “CEO’s Letter of Transmittal,” summarizing the performance of CalPERS, the largest public employee retirement system in the United States. Because what’s happening at CalPERS – they now pay more in benefits than they collect in contributions – is happening everywhere.

For the first time in history, America’s public employee pension funds, managing well over $4.0 trillion in assets, are becoming net sellers, not buyers. And as any attentive student of economics will tell you, when there are more sellers than buyers, prices drop. Behind this mega economic trend is a mega demographic trend – across the developed world, certainly including the United States, a relentlessly increasing percentage of the population is retired. The result? An increasing proportion of people who are retired and slowly liquidating their lifetime savings – also driving down asset values and investment returns.

Last week’s sell-off in the markets has immediate causes that get most of the attention. Turmoil in the middle east. A long overdue slowdown to China’s overheated economy. Depressed energy prices. But there are two long-term trends that will keep investment returns down. Demographics is one of them: The more retirees, the more sellers in the market. The other mega-trend, equally troubling to investors, is that debt accumulation, which stimulates spending, has reached its limit. We are at the end of a long-term, decades long credit cycle. The next three charts will illustrate the relationship between interest rates, debt formation, and the stock market during two critical periods – the first one following the stock market peak in December 1999, and the second following the stock market peak in September 2007.

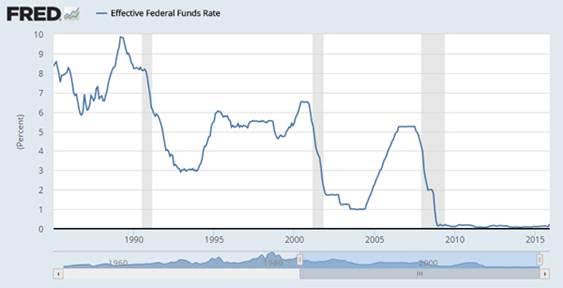

The first chart shows the federal funds rate over the past 30 years. As can be seen, when the stock market peaked in December 1999, the federal funds rate was 6.5%. Within three years, in order to stimulate borrowing which would put cash into the economy, that rate was dropped to 1.0%. Similarly, once the stock market recovered, the rate went back up to 4.25% until the stock market peaked again in the summer of 2007. Then as the market declined precipitously for the next 18 months through February of 2009, the federal funds rate was lowered to 0.15% and has stayed near that low ever since. The point? As the stock market recovered since February of 2009 to the present, unlike during the earlier recoveries, the federal funds rate was never raised. This time, there’s no elbow room left.

Effective Federal Funds Rate – 1985 to 2015

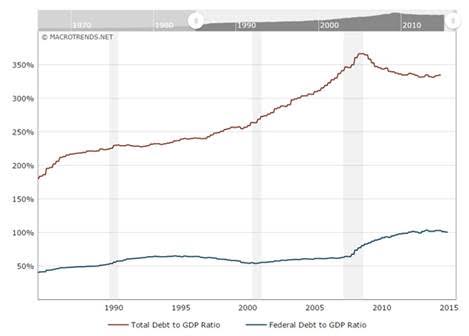

To put these low interest rates in context requires the next chart which shows total U.S. credit market debt as a percent of GDP over the past 30 years. Consumer debt, commercial debt, financial debt, state and federal debt (not including unfunded liabilities, by the way), is now estimated at 340% of U.S. GDP. The last time it was this high was 1929, and we know how that ended. As it is, even though interest rates have stayed at nearly zero for just over seven years, total debt accumulation topped out at 366.5% of GDP in February of 2009 and has slightly declined since then. The point here? Low interest rates, this time at or near zero, no longer stimulate a net increase in total borrowing, which in turn puts cash into the economy.

Total U.S. Credit Market Debt – 1985 to 2015

Which brings us to the Dow Jones Industrial Average, a stock index that tracks nearly in lockstep with the S&P 500 and the Nasdaq, and is therefore an accurate representation of the historical performance of U.S. equities over the past 30 years. As can be seen from this graph and the preceding graphs, the market downturn between December 1999 and September of 2002 was countered by lowering the federal funds rate from 6.5% to 1.0%. Later in the aughts, the market downturn between September 2007 to February 2009 was countered by lowering the federal funds rate from 5.25% to 0.15%. But during the sustained market rise for the seven years since then, the federal funds lending rate has remained at near zero, and total market debt as a percent of GDP has actually declined slightly.

Dow Jones Industrial Average – 1985 to 2015

{kind=link}

It doesn’t take a trained economist to understand that the investment landscape has fundamentally changed. The trend is clear. Over the past thirty years debt as a percent of GDP has doubled from 150% to over 350%, then remained flat for the past seven years. At the same time, over the past thirty years the federal lending rate has dropped high single digits in the 1980’s to pretty much zero by early 2009, and has remained there ever since. The conclusion? Interest rates can no longer be used as a tool to stimulate the economy or the stock market, and the capacity of the American economy to grow through debt accumulation has reached its limit.

For these reasons, achieving annual investment returns of 7.5%, or even 6.5%, for the next several years or more, is much harder, if not impossible. Conditions that stock market growth has relied on over the past 30 years no longer apply. Public employee pension funds, starting with CalPERS, need to face this new reality. Debt and demographics create headwinds that have changed the big picture.

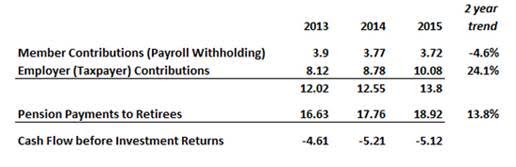

In the case of CalPERS, of course, it isn’t mere demographics that has turned them into a net seller in a market that’s just given up two years of appreciation. It’s the fact that their retiree population is increasingly comprised of people who are retiring with benefits that have been enhanced in the past 10-15 years. This fact accelerates and augments the demographically driven disparity between collections and disbursements. Take a look at the past three years of CalPERS collections and disbursements:

CalPERS Cash Flow (not including investment returns)

2013 to 2015, $=Billions

These figures, drawn from CalPERS 6-30-2015 CAFR (page 26) and CalPERS 6-30-2014 CAFR (page 24), show the system to be a net seller at a rate of about $5.0 billion per year for the past three years. Interestingly, during that time, employee contributions to CalPERS have actually declined by 4.6%, at the same time as the employer, or taxpayer, contributions have risen by 24.1%.

The idea that CalPERS cannot lobby for equitably reduced pension benefits is a fallacy. Because the financial problems with pensions began when Prop. 21 was narrowly passed in 1984, deleting constitutional restrictions and limitations on the purchase of corporate stock by public retirement systems. The financial problems got worse when California’s legislature passed SB 400 in 1999, which set the precedent for retroactive pension benefit increases. And in both cases, CalPERS was there, lobbying for passage of what were ultimately ruinous decisions.

Now that an aging population delivers millions of sellers into a market already challenged by epic deleveraging, CalPERS can do the right thing, and lobby for meaningful pension reform. They can start by supporting policies that reverse the impact of Prop. 21 and SB 400. If they do this sooner rather than later, they may be able to save the defined benefit. Anne Stausboll, are you prepared to stand up to your union controlled board of directors, and tell them the hard truth?

[divider] [/divider]

Originally posted at Fox & Hounds Daily.

Ed Ring is the executive director of the California Policy Center.